Why Property Insurance Is the Smart Move for Protecting What You’ve Built

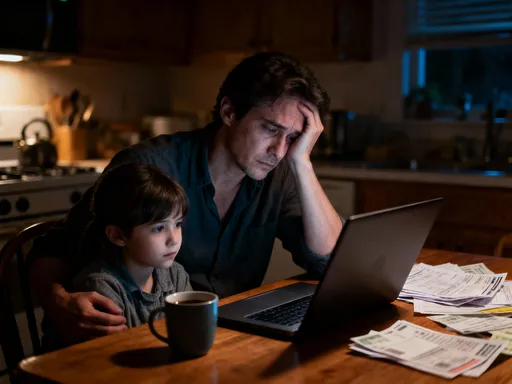

You work hard for your money—so why leave your biggest assets exposed? I’ve seen too many people overlook property insurance until it’s too late. It’s not just about covering a home; it’s about safeguarding years of effort. Think of it as a financial seatbelt. Without it, one unexpected event could undo everything. A storm, a fire, or even a visitor’s injury can lead to overwhelming expenses. The right property insurance doesn’t just pay for repairs—it preserves your financial stability, protects your savings, and ensures that a single incident doesn’t derail your long-term goals. Let me show you how the right coverage quietly works in the background, keeping your wealth intact.

The Reality Check: When “It Won’t Happen to Me” Backfires

It's natural to believe that disasters only happen to others. Many homeowners operate under the assumption that their neighborhood is too safe, their home too sturdy, or their luck too good for anything serious to occur. This mindset, known as optimism bias, leads people to downplay real risks. Yet statistics tell a different story. According to data from the Federal Emergency Management Agency (FEMA), more than 90% of natural disasters in the United States involve some form of flooding, and nearly every county has experienced a federally declared disaster in the past decade. Despite this, only about 12% of homeowners carry flood insurance. When a pipe bursts during winter or a tree crashes through a roof in a storm, the financial shock can be paralyzing.

Consider the case of a family in the Midwest who skipped comprehensive coverage to save on premiums. After a summer thunderstorm brought high winds, a large oak tree fell onto their house, collapsing part of the roof and damaging the attic and two bedrooms. Without adequate insurance, they faced over $40,000 in repairs. Their emergency fund, meant for college savings and retirement contributions, was drained in months. The emotional toll was just as heavy—stress over bills, strained relationships, and the loss of peace of mind. This is not an isolated incident. Every year, thousands of households experience similar setbacks, not because they were careless, but because they underestimated the likelihood of loss.

The truth is, no amount of caution eliminates risk entirely. You can install the best locks, maintain your roof diligently, and live in a low-crime area, but external events—like wildfires spreading due to dry conditions or a neighbor’s uninsured driver crashing into your garage—are beyond your control. Property insurance doesn’t promise to prevent accidents, but it does provide a financial buffer when they occur. Ignoring coverage in the name of frugality is not thrift—it’s a gamble with everything you’ve built. And unlike investments, where risk can be measured and diversified, this gamble offers no upside. The cost of being wrong is total loss. Recognizing this reality is the first step toward responsible financial planning.

What Property Insurance Really Covers (And What It Doesn’t)

At its core, a standard homeowners insurance policy is designed to protect against sudden and accidental damage to your home and personal property. Most policies include four key components: dwelling coverage, personal property protection, liability insurance, and additional living expenses. Dwelling coverage pays to repair or rebuild the physical structure of your home if it’s damaged by covered perils like fire, windstorms, or vandalism. Personal property coverage helps replace belongings—furniture, electronics, clothing—that are stolen or destroyed. Liability protection kicks in if someone is injured on your property and decides to sue, covering legal fees and medical costs. Additional living expenses, sometimes called loss of use coverage, helps pay for hotel stays, meals, and other costs if your home becomes uninhabitable during repairs.

However, not all risks are included. Standard policies typically exclude damage caused by floods, earthquakes, and sewer backups. These exclusions exist because such events are either geographically concentrated or carry high potential costs. For example, flood damage is not covered under a typical homeowners policy, even if it results from heavy rain overwhelming local drainage systems. Homeowners in flood-prone areas are often required by lenders to purchase separate flood insurance through the National Flood Insurance Program (NFIP) or a private insurer. Similarly, earthquake coverage must be added as an endorsement or purchased as a standalone policy, especially in regions with higher seismic activity. Failing to recognize these gaps can lead to devastating surprises when filing a claim.

Another common misconception is that insurance covers routine wear and tear. It does not. If your roof leaks because it’s 20 years old and deteriorating, that’s considered maintenance, not a covered loss. Insurance is meant for unexpected events, not gradual decline. This is why understanding your policy’s language is essential. Terms like “replacement cost” and “actual cash value” have significant financial implications. Replacement cost coverage pays to rebuild or replace an item at today’s prices, without deducting for depreciation. Actual cash value, on the other hand, factors in depreciation, meaning you may receive far less than it costs to replace an item. Choosing the right type of coverage ensures you’re not left paying the difference out of pocket.

To avoid confusion, experts recommend reviewing your policy annually and asking your agent to walk you through each section. Request a detailed explanation of exclusions and consider whether additional endorsements—such as scheduled personal property coverage for high-value items like jewelry or art—are necessary. Clarity today prevents disputes tomorrow. Knowledge is not just power; in the context of insurance, it’s financial protection.

How the Right Coverage Preserves Your Net Worth

Your home is likely your single largest financial asset. For most families, it represents decades of mortgage payments, home improvements, and market appreciation. Losing equity due to an uninsured disaster can set back financial progress by years, if not decades. Property insurance acts as a shield, ensuring that sudden losses don’t erode your net worth. Consider two homeowners: one fully insured, the other underinsured. Both experience a kitchen fire that causes $75,000 in structural and content damage. The insured homeowner files a claim, pays a $2,500 deductible, and receives a settlement that covers repairs and replacement of belongings. Their financial life continues largely uninterrupted. The underinsured homeowner, lacking sufficient coverage, must cover $50,000 in costs personally. They dip into retirement accounts, take on high-interest loans, or sell investments at an inopportune time—each decision weakening their long-term financial foundation.

Insurance doesn’t just cover immediate costs; it prevents a chain reaction of financial strain. Without protection, families may delay retirement, reduce college savings, or abandon investment plans to cover unexpected expenses. A study by the Insurance Information Institute found that nearly 40% of uninsured homeowners facing major property damage reported a significant negative impact on their credit score within a year. In contrast, those with adequate coverage maintained financial stability and continued building wealth. This difference underscores a crucial point: wealth accumulation isn’t only about earning and investing—it’s also about protecting what you already have.

Moreover, lenders require homeowners insurance as a condition of the mortgage. If you fail to maintain coverage, your lender may purchase force-placed insurance, which is often more expensive and offers less protection. This not only increases your monthly costs but also puts your loan in jeopardy. Beyond compliance, having robust insurance allows you to leverage your home equity confidently—whether for home improvements, education funding, or investment opportunities—knowing that your asset is protected. In this way, insurance becomes an enabler of growth, not just a safety net.

From a broader financial planning perspective, insurance fits into the principle of risk pooling. By paying a predictable, manageable premium, you transfer the risk of a catastrophic loss to an insurer. This allows you to allocate capital more efficiently—investing in stocks, bonds, or a business—without the constant fear of losing everything to an unforeseen event. The peace of mind that comes with knowing your home is protected is invaluable, but the financial benefit is measurable: sustained net worth, uninterrupted savings, and continued progress toward long-term goals.

Avoiding Overpayment: Smart Ways to Optimize Premiums

While having enough coverage is essential, paying too much for it undermines its value. Many homeowners overpay simply because they don’t review their policies or shop around. Insurance premiums can vary significantly between providers, even for identical coverage. A J.D. Power study found that consumers who compared quotes saved an average of 22% on their annual premiums. This means a typical homeowner paying $1,500 per year could save $330 annually—money that could go toward retirement, education, or emergency savings. The key is treating insurance like any other financial product: one that should deliver value for the price.

One of the most effective ways to reduce premiums is bundling. Many insurers offer discounts of 10% to 25% when you combine homeowners and auto insurance with the same company. These multi-policy discounts are widely available and easy to implement. Another strategy is adjusting your deductible. Raising your deductible from $500 to $1,000 can lower your premium by 10% to 25%, depending on the insurer and location. This only makes sense if you have enough in emergency savings to cover the higher out-of-pocket cost if a claim arises. For financially disciplined households, this trade-off is often worthwhile.

Improving home safety and security can also lead to discounts. Installing a monitored security system, deadbolts, smoke detectors, or a fire sprinkler system may qualify you for reductions of up to 15%. Some insurers even offer discounts for homes with updated electrical, plumbing, or roofing systems—features that reduce the likelihood of claims. If you’ve made improvements since your policy began, inform your insurer. They may not automatically know about upgrades that lower risk.

Additionally, loyalty isn’t always rewarded. Staying with the same insurer for years may feel comfortable, but it doesn’t guarantee the best rate. Insurers often offer lower introductory rates to new customers, meaning long-term policyholders may be paying more than necessary. Conducting an annual review—comparing your current policy to at least two other quotes—ensures you’re not overpaying. Some insurers also offer paperless billing, automatic payments, or loyalty bonuses, so ask about all available discounts. The goal is not to chase the cheapest policy, but to find the best value: adequate coverage at a fair price.

The Hidden Risks Everyone Ignores

When people think of property damage, they often imagine dramatic events like fires or hurricanes. But some of the most common—and costly—claims stem from quieter, everyday risks. Water damage from burst pipes, for example, accounts for nearly 20% of all homeowners insurance claims, according to the Insurance Information Institute. A small leak under a sink, left undetected for weeks, can lead to mold growth, structural damage, and thousands in repairs. Similarly, sump pump failures during heavy rains can flood basements, ruining furniture, appliances, and personal belongings. These incidents are often preventable, but without proper coverage, the financial burden falls entirely on the homeowner.

Liability risks are another overlooked area. Imagine a guest slips on a wet floor and breaks a wrist. Medical bills can quickly exceed $20,000, and if they sue, legal fees could add tens of thousands more. Standard liability coverage typically starts at $100,000, but experts recommend at least $300,000—and often $500,000 or more, especially for homeowners with significant assets. Without enough coverage, your savings and future earnings could be at risk in a judgment. Umbrella insurance, which provides extra liability protection beyond your homeowners policy, is an affordable way to close this gap, often costing less than $200 per year for $1 million in coverage.

Other hidden risks include damage from power surges, which can destroy electronics and appliances, or losses due to identity theft related to stolen personal documents. Some policies offer endorsements for these scenarios, but they’re not included by default. Even dog ownership can pose a liability risk; certain breeds may lead to higher premiums or exclusions. The point is, risk evolves as your life changes. A home office, rental of a spare room, or installation of a swimming pool all introduce new exposures that may require policy adjustments.

To stay protected, conduct a home risk audit at least once a year. Walk through each room, identify potential hazards—like old wiring or slippery stairs—and assess whether your coverage matches your current lifestyle. Speak with your agent about any changes in your household, possessions, or property use. Insurance should be a dynamic part of your financial plan, not a static document filed away after closing. By staying proactive, you avoid the shock of discovering a gap when it’s too late.

Working With Insurers Like a Pro: Claims, Negotiations, and Documentation

Filing a claim should be a straightforward process, but without preparation, it can become stressful and frustrating. The difference between a smooth resolution and a denied claim often comes down to documentation and communication. The first step after a loss is to ensure safety—evacuate if necessary, secure the property, and contact emergency services. Then, notify your insurer as soon as possible. Most companies have 24/7 claims hotlines and online portals to streamline reporting.

When the adjuster arrives, be present and prepared. Have your policy number, a list of damaged items, and photos or videos of the damage ready. Before any repairs begin, document everything: take wide-angle shots of each affected room, close-ups of damaged areas, and inventory lists with estimated values. This evidence strengthens your claim and reduces the chance of disputes. A home inventory—a detailed list of your belongings with descriptions, purchase dates, and receipts—is invaluable. Apps and online tools can help you create and store this digitally, with cloud backups for added security.

Be honest but strategic in your communication. Adjusters are trained to assess damage fairly, but they also represent the insurer’s interests. If you believe the initial offer is too low, you have the right to appeal. Gather repair estimates from licensed contractors, provide receipts for replaced items, and request a re-evaluation. Most insurers will reconsider with additional evidence. In complex cases, hiring a public adjuster—someone who works for you, not the insurer—can help maximize your settlement, though they typically charge a fee based on the claim amount.

Keep all correspondence in writing and follow up regularly. Don’t accept the first offer if it doesn’t reflect the full cost of recovery. At the same time, avoid exaggerating losses, as this can lead to fraud investigations and policy cancellation. The goal is a fair and accurate settlement that allows you to rebuild without financial strain. By approaching the process with organization and confidence, you turn a potentially overwhelming experience into a manageable one.

Insurance as a Core Pillar of Long-Term Financial Health

True financial success isn’t measured only by income or investment returns—it’s also defined by resilience. The ability to withstand setbacks without derailing your goals is what separates sustainable wealth from temporary prosperity. Property insurance is not a luxury or an afterthought; it’s a foundational element of responsible financial planning. Just as you diversify investments to manage market risk, you insure your home to manage physical and liability risks. Both are essential strategies for preserving capital.

When you view insurance as a proactive tool rather than a reactive expense, your entire financial mindset shifts. Instead of seeing premiums as money lost, you recognize them as a cost of protection—similar to maintenance on a car or regular health checkups. These are not expenses that generate immediate returns, but they prevent far greater losses down the road. Over time, this disciplined approach compounds: you avoid debt, maintain credit health, and continue investing toward your goals without interruption.

Moreover, having comprehensive coverage contributes to peace of mind, which is itself a form of wealth. Knowing that your family, home, and belongings are protected allows you to focus on what matters—raising children, pursuing passions, and building a meaningful life. Financial stress is a leading cause of anxiety and relationship strain; reducing that burden through smart planning improves overall well-being.

In the end, property insurance is about more than replacing shingles or repairing walls. It’s about honoring the effort, sacrifice, and vision that went into building your life. It’s about ensuring that one storm, one accident, one moment of bad luck doesn’t erase years of progress. By making insurance a non-negotiable part of your financial strategy, you take control of your future. You stop gambling with your assets and start protecting them with intention. That’s not just smart—it’s essential.