How I Turned Investment Losses into Tax Wins — Smart Moves After the Market Dropped

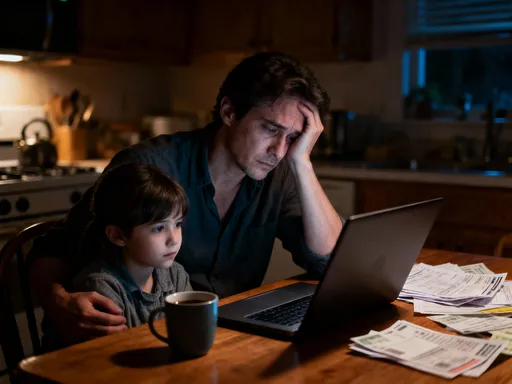

Losing money in the market stings — I’ve been there. But what if those losses could actually save you money? After a tough year of downturns, I discovered how smart tax optimization can soften the blow. It’s not about chasing returns; it’s about minimizing damage and working the system fairly. This is how I restructured my strategy, legally reduced my tax burden, and turned setbacks into strategic advantages — and how you might too. While no one enjoys seeing their portfolio shrink, understanding the tax implications of investment losses can transform disappointment into opportunity. The key lies not in avoiding losses altogether — that’s impossible — but in using them wisely within the framework of the tax code.

When the Market Crashes, Your Portfolio Isn’t the Only Thing at Risk

When stock prices fall sharply, the immediate reaction for many investors is fear. Seeing account balances decline can trigger emotional responses that lead to impulsive decisions. One of the most common mistakes during a market downturn is panic selling — liquidating investments at a loss without considering the broader financial picture. While it may feel like regaining control, this move often locks in losses unnecessarily and can disrupt long-term investment goals. More importantly, few investors pause to consider how these losses might be used constructively within their tax planning.

The psychological impact of market drops should not be underestimated. For individuals managing household finances or saving for long-term goals like children’s education or retirement, a sudden decline can feel destabilizing. However, experienced investors understand that volatility is part of the cycle. Instead of reacting emotionally, they assess whether the fundamentals of their holdings have changed. If not, a temporary price drop may represent a buying opportunity rather than a reason to exit. Yet beyond rebalancing or holding steady, there’s another layer most overlook: the potential tax benefits embedded in realized losses.

This shift in perspective — from seeing losses purely as failures to recognizing them as tools — changes everything. Tax laws in many countries, including the United States, allow investors to use capital losses to offset gains, thereby reducing taxable income. This means that even in a bad year, there are mechanisms to limit financial damage. But to access these benefits, investors must act deliberately and with knowledge. Acting out of emotion bypasses these opportunities entirely. By staying calm and informed, you position yourself to make decisions that serve both your immediate tax situation and your long-term wealth strategy.

Moreover, the timing of sales matters greatly. Selling an underperforming asset late in the year versus early the next can affect which tax period the loss applies to. Investors who act hastily may miss optimal windows for tax-loss harvesting. Understanding this timing element allows for more precise planning. It also underscores the importance of viewing investment performance through a dual lens: financial return and tax efficiency. When both are considered, what looks like a setback on the surface can become a stepping stone toward greater fiscal responsibility.

The Hidden Benefit No One Talks About: Tax-Loss Harvesting

Among the most powerful yet underutilized strategies in personal finance is tax-loss harvesting. At its core, tax-loss harvesting involves selling investments that have declined in value to realize a capital loss. That loss can then be used to offset capital gains from other parts of the portfolio, effectively lowering the amount of taxable income. While it won’t restore the lost principal, it can significantly reduce the tax bill, making the financial sting less severe. For many investors, especially those in higher tax brackets, this strategy can result in thousands of dollars in savings over time.

To understand how this works, it’s important to distinguish between short-term and long-term capital gains. Short-term gains apply to assets held for one year or less and are taxed at ordinary income rates, which can be as high as 37% depending on income level. Long-term gains, from assets held more than a year, are taxed at lower rates — typically 0%, 15%, or 20%. Losses are first applied against gains of the same type: short-term losses offset short-term gains, and long-term losses offset long-term gains. Any remaining net loss can then be used to offset the other type of gain.

For example, suppose an investor realizes $8,000 in short-term gains from selling a tech stock but also sells a struggling retail stock at a $5,000 loss. That loss directly reduces the taxable gain to $3,000, resulting in a much smaller tax liability. If total losses exceed total gains in a given year, up to $3,000 of the excess loss can be deducted against ordinary income — such as wages or interest income. This provides additional relief even in years when no gains were realized.

What makes tax-loss harvesting particularly effective is its repeatability. Because markets move in cycles, downturns will inevitably occur again. Investors who learn to implement this strategy consistently can build a habit of turning market volatility into tax advantage. It does not require speculative behavior or complex financial instruments — only careful tracking and disciplined execution. Over decades, the cumulative effect of saving even a few hundred dollars annually through loss harvesting can compound into meaningful wealth preservation.

However, the strategy is not automatic. It requires active monitoring of portfolio performance, awareness of tax rules, and a willingness to make tactical adjustments. Some investors rely on robo-advisors that automate tax-loss harvesting, while others work with financial advisors to execute it manually. Regardless of method, the principle remains the same: use losses strategically rather than letting them go to waste. In doing so, you transform passive suffering into active financial management.

Avoiding the Wash Sale Rule Trap — A Costly Mistake

One of the biggest pitfalls in tax-loss harvesting is inadvertently violating the wash sale rule. This IRS regulation disallows the deduction of a capital loss if you buy a “substantially identical” security within 30 days before or after the sale. The purpose of the rule is to prevent investors from selling an asset solely to claim a tax loss while maintaining economic exposure by repurchasing it almost immediately. If triggered, the loss is not lost forever but is instead added to the cost basis of the new purchase, delaying the tax benefit until that position is eventually sold.

While the rule seems straightforward, many investors fall into the trap unintentionally. For instance, someone might sell a mutual fund tracking the S&P 500 to harvest a loss, then reinvest in an ETF that tracks the same index just a week later. Though the fund and ETF are different vehicles, they are considered substantially identical due to nearly identical holdings and performance. Similarly, switching between share classes of the same fund — such as Class A and Class C shares — won’t circumvent the rule either.

The consequences can be significant. An investor who thought they had reduced their taxable income by $10,000 might discover during tax season that the IRS disallowed the loss, leaving them with a higher-than-expected tax bill. Worse, if the mistake goes unnoticed, it could lead to penalties or audits down the line. Therefore, understanding what constitutes a “substantially identical” security is critical to preserving the integrity of your tax strategy.

That said, there are smart ways to maintain market exposure without triggering the wash sale rule. One approach is to invest in a similar but not identical asset. For example, after selling a large-cap U.S. stock fund, you might purchase a fund focused on large-cap value stocks or one with slight differences in sector weighting. Another option is to temporarily allocate the proceeds into a broader market index fund while waiting out the 31-day window. These moves keep capital working in the market while complying with IRS requirements.

For investors managing multiple accounts — such as individual taxable accounts, joint accounts, or IRAs — extra caution is needed. The wash sale rule applies across all accounts owned by the taxpayer. This means selling a stock at a loss in a brokerage account and buying it back in an IRA within the 30-day window still violates the rule, even though IRAs are tax-advantaged. Many people are unaware of this cross-account application, making it a silent risk in otherwise well-planned strategies.

Pairing Losses with Gains: The Art of Strategic Offsetting

Not all capital gains are taxed equally, and neither should all losses be treated the same way. The most tax-efficient use of losses is to offset short-term gains first, since those are taxed at higher ordinary income rates. By strategically pairing a realized loss with a high-taxed gain, investors maximize the dollar-for-dollar tax savings. This prioritization ensures that the benefit of the loss is felt where it matters most — in reducing the heaviest tax burdens.

Imagine an investor who has $6,000 in short-term gains and $4,000 in long-term gains. They also have $7,000 in realized capital losses. Applying the $6,000 of loss to the short-term gain eliminates the highest-taxed portion first, leaving $1,000 to offset part of the long-term gain. The remaining $3,000 in long-term gain is taxed at a lower rate, resulting in a significantly reduced overall tax bill. If the same investor had applied the loss in reverse order, the tax savings would be smaller.

When losses exceed gains in a given year, the excess can be carried forward indefinitely to offset future gains. This feature adds long-term flexibility to tax planning. A particularly rough market year might generate substantial losses that can be preserved for use in more prosperous years when capital gains are realized. This smoothing effect helps stabilize tax liabilities over time, avoiding spikes in tax payments during strong market cycles.

Keeping accurate records is essential to effective loss carryforward. Investors must track the amount of unused losses each year and report them correctly on tax returns. Software platforms and tax preparers can assist with this, but the responsibility ultimately lies with the taxpayer. Failing to carry forward losses properly means leaving money on the table — a preventable oversight that undermines years of careful investing.

Another consideration is the interaction between capital losses and other forms of income. As mentioned earlier, up to $3,000 in net capital losses can be deducted against ordinary income annually. For individuals facing job loss, reduced hours, or retirement, this deduction can provide welcome relief. It also makes tax-loss harvesting valuable even in years with no capital gains. The ability to reduce taxable income from wages, pensions, or self-employment earnings enhances the versatility of the strategy.

Beyond Stocks: Applying Tax Optimization Across Asset Types

While stocks are the most visible component of many portfolios, tax-loss harvesting applies to a wide range of investment vehicles. Mutual funds, exchange-traded funds (ETFs), bonds, and even cryptocurrency are all subject to capital gains and losses, meaning the same principles of tax optimization can be applied. Diversified investors stand to gain the most by taking a holistic view of all taxable accounts and identifying loss opportunities across asset classes.

Mutual funds and ETFs are common candidates for tax-loss harvesting, especially when fund performance lags due to sector rotation or management changes. Because these funds hold baskets of securities, their value can decline even if individual holdings perform well. Selling a losing fund to realize a loss — while avoiding the wash sale rule by choosing a non-identical alternative — allows investors to maintain diversification while gaining tax benefits.

Bonds, though generally less volatile than stocks, can also experience price declines, particularly when interest rates rise. An investor who bought a long-term bond fund when rates were low may see a paper loss when rates increase. Selling such a position to harvest a loss is a valid strategy, especially if reinvesting in a shorter-duration bond fund or waiting to re-enter the market. Bond losses can offset bond gains or stock gains, contributing to overall tax efficiency.

Cryptocurrency introduces additional complexity due to its unique regulatory treatment, but the basic rules of capital gains and losses still apply. If an investor sells Bitcoin at a loss after holding it for less than a year, that loss can offset short-term gains elsewhere. Given the high volatility of digital assets, crypto investors may find frequent opportunities for tax-loss harvesting, though they must keep meticulous records due to the decentralized nature of transactions.

Rebalancing a portfolio offers a natural opportunity to implement tax-loss harvesting. As markets shift, asset allocations drift from target weights. Selling overweight positions that have appreciated and buying underweight ones that have declined can restore balance while generating tax advantages. When done with tax implications in mind, rebalancing becomes not just a risk management tool but a tax-saving event.

Working with the System: Timing, Accounts, and Long-Term Planning

Tax optimization is not a one-time event but an ongoing process integrated into wealth management. Timing plays a crucial role. Most investors review their portfolios toward year-end, making November and December prime months for identifying tax-loss harvesting opportunities. Acting early enough allows time to assess positions, execute trades, and ensure settlements occur before December 31 — a key deadline for tax reporting.

Understanding the difference between taxable and tax-advantaged accounts is equally important. Tax-loss harvesting only applies to taxable brokerage accounts, not retirement accounts like IRAs or 401(k)s. Within retirement accounts, all transactions are tax-deferred or tax-free, so there is no opportunity to claim capital losses. This makes the management of taxable accounts especially critical for high-net-worth individuals with significant investments outside retirement plans.

Long-term planning enhances the effectiveness of tax strategies. For example, retirees drawing down portfolios may realize gains from selling appreciated assets. Having a reserve of carried-forward losses can offset these gains, preserving more income for spending. Similarly, parents transferring assets to children or setting up education funds can time gifting strategies around capital gain events to minimize tax impact.

Integrating tax awareness into investment decisions fosters resilience. Instead of fearing downturns, investors learn to anticipate them as part of the cycle. This mindset shift reduces stress and promotes discipline. It also aligns with broader financial goals, such as funding retirement, supporting family, or building legacy wealth. Tax-smart investing doesn’t chase quick wins; it builds enduring stability.

When to Seek Help — And When to Trust Your Instincts

While tax-loss harvesting is accessible to many investors, complex situations call for professional guidance. Those with large portfolios, multiple account types, or international holdings may benefit from consulting a certified public accountant (CPA) or fee-only financial advisor. Tax laws change frequently, and missteps can be costly. A qualified professional can help navigate nuances like cost basis reporting, wash sale tracking, and coordination across accounts.

There are also red flags to watch for. Be cautious of strategies that promise guaranteed tax savings or involve aggressive interpretations of the rules. The goal is not to evade taxes but to minimize liabilities within legal boundaries. Ethical, sustainable planning builds trust and protects your financial future. If a strategy feels too clever or complicated, it may carry hidden risks.

That said, investors should not feel powerless. Basic tax-loss harvesting can be managed independently with careful recordkeeping and access to reliable tools. Many brokerage platforms now offer dashboards that highlight potential loss candidates and track wash sale risks. With education and attention to detail, even novice investors can begin incorporating tax efficiency into their approach.

Ultimately, financial empowerment comes from knowledge. Understanding how the system works allows you to make informed choices rather than reacting out of fear or confusion. Whether you decide to manage taxes yourself or work with a professional, the most important step is awareness — knowing that losses are not the end of the story, but part of a larger financial narrative.

Turning Setbacks into Stepping Stones

Losses are inevitable in investing — but they don’t have to be defeats. With the right mindset and tools, they can become powerful levers for financial efficiency. Tax optimization isn’t about gaming the system; it’s about understanding it and using every legal avenue to protect your wealth. By treating downturns as part of the cycle, not the end of the road, you gain control, reduce stress, and build resilience. The smartest move after a loss? Looking beyond the number and seeing the opportunity beneath. In the quiet aftermath of a market drop lies a chance to act with clarity, purpose, and foresight. That’s how setbacks become stepping stones — not just for saving on taxes, but for building a smarter, stronger financial future.