How I Navigated High School Costs Without Losing My Mind

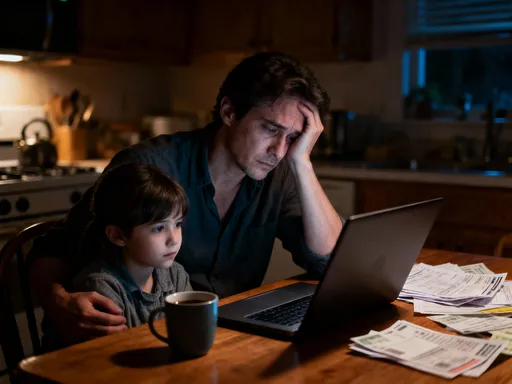

Paying for high school shouldn’t feel like a financial trap. Yet between supplies, extracurriculars, and unexpected fees, costs add up fast. I’ve been there—stressed, overwhelmed, and unsure where to cut back. That’s why I started tracking every expense and testing practical money-saving methods. What worked surprised me. This guide shares real strategies that helped my family stay on track—without sacrificing quality or peace of mind. It’s not about living with less; it’s about making smarter choices, planning ahead, and protecting your family’s financial stability during one of life’s most demanding phases. The journey begins with awareness, and ends with control.

The Hidden Price of High School Education

Many parents operate under the assumption that public high school is free, but the reality tells a different story. While tuition may not appear on a monthly bill, the associated costs can quietly accumulate into a significant financial burden. Textbooks, technology requirements such as laptops or tablets, transportation fees, and school uniforms are just the beginning. Standardized testing like the SAT or ACT comes with registration fees, prep materials, and sometimes travel expenses. These are not one-time costs; they recur each year, and in some cases, increase with grade level. By the time a student reaches senior year, the total out-of-pocket spending can rival a small college semester’s expenses—and that’s before considering extracurriculars.

Extracurricular activities, often marketed as essential for college applications, carry their own price tags. Sports teams require equipment, travel, and participation dues. Band or theater programs may involve instrument rentals, costume fees, and overnight trips. Academic clubs like robotics or science Olympiad often need materials, competition entry fees, and chaperone costs. Field trips, while educational, can cost anywhere from $25 to several hundred dollars depending on destination and duration. A single class project might require supplies that aren’t covered by the school budget. These expenses, though individually small, form a cumulative weight that many families are unprepared for.

The timing of these costs often compounds the strain. Fees tend to surface at the start of semesters or before major events, creating cash flow challenges. A family might manage monthly bills comfortably but struggle when faced with a $300 robotics competition fee in March. Without a dedicated savings plan, such expenses force difficult trade-offs—delaying car repairs, cutting back on groceries, or relying on credit cards. Middle-income households, who don’t qualify for many assistance programs but lack the cushion of higher earners, are especially vulnerable. The lack of transparency around these costs means many parents only discover them when invoices arrive, leaving little time to adjust.

Understanding the full scope of high school expenses is the first step toward regaining control. It’s not about fear, but foresight. By mapping out anticipated costs over four years, families can shift from reactive spending to proactive planning. This awareness transforms financial stress into strategic decision-making. Knowing what to expect allows for better budgeting, smarter saving, and more confident conversations with school administrators about support options. The goal isn’t to eliminate all costs—many are worthwhile investments in a child’s education—but to approach them with intention, not surprise.

Building a Realistic Education Budget (And Actually Sticking to It)

A budget is not a punishment; it’s a roadmap. When it comes to high school expenses, the most effective budgets are not rigid spreadsheets that crumble at the first unexpected fee, but flexible plans built with realism and adaptability in mind. The foundation lies in categorizing expenses: predictable, recurring costs versus variable, situational ones. Predictable costs include annual fees, textbook rentals, transportation passes, and standardized testing schedules. These can be anticipated and allocated for months in advance. Variable costs, such as class projects, last-minute field trips, or club dues, require a different approach—one that includes buffer zones and emergency reserves.

Creating this budget starts with gathering information. Review past school bills, talk to other parents, and consult school handbooks to compile a comprehensive list of potential expenses. Organize them by academic year and by semester. Assign conservative estimates to variable costs based on previous years’ data. Once the full picture emerges, divide the total by 12 to determine a monthly savings target. For example, if estimated high school costs over four years total $8,000, that’s about $167 per month. Setting up an automatic transfer to a dedicated savings account ensures consistency without constant decision-making.

One of the most powerful yet underused tools in budgeting is involving teenagers in the process. When teens understand how much a prom ticket or a sports uniform costs, and see it reflected in the family’s financial plan, they develop a sense of responsibility. This doesn’t mean burdening them with adult stress, but inviting them into age-appropriate conversations about trade-offs. For instance, if they want to join a costly club, discuss how that might affect other spending choices. This builds financial literacy in real time, turning abstract concepts like budgeting and prioritization into lived experience.

Sticking to the budget requires regular check-ins. Monthly reviews allow families to assess what’s working and what needs adjustment. Digital tools like budgeting apps with envelope-style categories can help visualize spending limits. Some families use separate savings sub-accounts for different goals—one for supplies, one for activities, one for emergencies. The key is consistency and communication. When everyone understands the plan and their role in it, adherence becomes a shared effort rather than a top-down restriction. Over time, this practice fosters a culture of financial awareness that extends far beyond high school.

Smart Savings Tactics That Actually Work

Saving for high school doesn’t require drastic lifestyle changes or extreme frugality. The most effective strategies are simple, repeatable, and sustainable over time. They rely not on deprivation, but on redirection and awareness. One of the most impactful methods is channeling small windfalls into dedicated education funds. Tax refunds, birthday money from relatives, or modest bonuses can be automatically deposited into a savings account before they’re spent. Even $200 from a tax credit, when saved consistently over four years, grows into a meaningful cushion.

Another practical tactic is leveraging cash-back apps and rewards programs for school-related purchases. Buying supplies at major retailers often qualifies for rebates through apps that scan receipts. Some credit cards offer bonus points on office supply or educational spending, which can be redeemed for statement credits or gift cards. These tools don’t change daily spending habits but enhance their value. The key is consistency—using the same app every time, scanning every receipt, and reinvesting the rewards rather than treating them as extra spending money.

Purchasing gently used items is another area where families can save without sacrificing quality. Uniforms, in particular, are often resold in excellent condition after a single school year. Many schools host used uniform exchanges or online parent groups where clothing is traded or sold at a fraction of retail prices. Textbooks, especially non-standard editions, can often be borrowed from older siblings or found used online. Even laptops and calculators, when properly maintained, can be passed down or purchased secondhand with full functionality.

Resource sharing within communities also yields significant savings. Families with multiple children in the same school can rotate supplies, split the cost of large items like scientific calculators or art kits, or carpool to reduce transportation expenses. Group orders for class projects or club materials often unlock bulk discounts. These cooperative efforts not only reduce costs but strengthen community ties. The underlying principle is efficiency: getting the same educational value at a lower financial cost. When these small actions are repeated year after year, they compound into thousands of dollars saved—funds that can be redirected toward future goals like college or emergency needs.

Earning Power: Side Opportunities for Families

When saving alone isn’t enough, generating additional income becomes a necessary strategy. For many families, the idea of taking on extra work feels overwhelming, but there are ethical, manageable ways to earn supplemental income without sacrificing family time or well-being. The key is identifying opportunities that align with existing skills, schedules, and resources. These aren’t about getting rich quickly, but about creating steady, reliable streams of income that directly support educational expenses.

Freelance work has become increasingly accessible thanks to digital platforms. Parents with skills in writing, graphic design, bookkeeping, or tutoring can find short-term projects that fit around school hours. Even a few hours of work per week can generate enough to cover a semester’s activity fees. Tutoring, in particular, offers a dual benefit: it supports other students while reinforcing the tutor’s own knowledge. Many schools and community centers welcome qualified volunteers or paid instructors for after-school programs.

Seasonal income opportunities also play a valuable role. Hosting a yard sale in the spring can turn unused household items into cash. With careful planning, a single weekend event can raise several hundred dollars. Online marketplaces make it easier than ever to sell gently used electronics, furniture, or children’s clothing. Renting out unused space, such as a garage or spare room, through legitimate platforms can provide monthly income with minimal effort. While not feasible for everyone, these options demonstrate how underutilized assets can become financial resources.

For teenagers, part-time jobs offer more than just money—they teach responsibility, time management, and the value of work. Jobs like tutoring younger students, pet sitting, lawn care, or working at local retail or food establishments provide real-world experience. Earnings can be directed toward personal expenses like phone bills, clothing, or entertainment, freeing up family funds for larger educational costs. Parents can support this by helping teens create a simple earnings plan, perhaps matching a portion of their savings as an incentive. This collaborative approach reinforces financial discipline while fostering independence.

Navigating Financial Aid and School-Based Support

One of the most overlooked resources for managing high school costs is the support already available through schools and local programs. Many families assume they don’t qualify for assistance or feel uncomfortable asking for help, but numerous options exist for those willing to inquire. Fee waivers, for example, are often available for standardized tests, application fees, and even certain extracurricular activities. These are not handouts, but formal programs designed to ensure equal access to educational opportunities regardless of income level.

Schools frequently offer subsidized meal plans for families who meet income guidelines. While often associated with younger students, these benefits extend into high school and can significantly reduce monthly grocery expenses. Textbook lending libraries allow students to borrow required materials for free, eliminating the need for costly purchases. Some districts provide laptops or tablets to students who lack reliable access at home. Free or low-cost tutoring services, either during school hours or through after-school programs, can reduce the need for private instruction.

Accessing these resources begins with communication. Speaking respectfully with school counselors, administrators, or financial officers opens the door to available support. Most educators understand that financial hardship is not a reflection of character, and many schools have discreet processes for assessing need. The conversation doesn’t have to be detailed—a simple statement like “We’re experiencing financial constraints and would like to know what assistance is available” is often enough to trigger a helpful response.

Community organizations also play a vital role. Local nonprofits, religious institutions, and civic groups sometimes offer grants or scholarships for specific needs like prom attire, senior portraits, or graduation expenses. These programs are often underpublicized, so proactive research is essential. Checking community bulletin boards, attending school events, or joining parent networks can uncover hidden opportunities. The goal is not to eliminate personal responsibility, but to use all available tools to reduce unnecessary financial strain. Transparency, not shame, is the foundation of effective support-seeking.

Avoiding Common Money Traps and Emotional Spending

Financial stress during high school years can lead to poor decision-making, especially when emotions run high. One of the most common pitfalls is overspending to maintain social parity. Parents may feel pressure to enroll their child in every activity, buy the latest uniform styles, or say yes to every field trip to avoid embarrassment. This “keeping up” mentality can quickly erode a budget and lead to resentment. The reality is that every family has different financial realities, and making intentional choices is not a sign of failure, but of wisdom.

Another dangerous trap is relying on high-interest credit to cover school-related expenses. Using credit cards for fees, supplies, or trips may solve an immediate problem, but it often leads to long-term debt if balances aren’t paid quickly. Interest charges can double the cost of a $200 fee within a year if only minimum payments are made. Payday loans or financing offers with hidden fees should be avoided entirely. These products are designed to exploit financial urgency and can trap families in cycles of repayment that are difficult to escape.

Emotional spending also surfaces during unexpected bills. A sudden $150 lab fee or a required software subscription can trigger panic, leading to impulsive decisions. To counter this, families should adopt a “cooling-off” rule for non-urgent purchases. Instead of reacting immediately, take 24 to 48 hours to research alternatives, check the budget, or explore assistance options. This pause allows for rational decision-making rather than stress-driven choices.

Equally important is building an emergency buffer specifically for education surprises. Even a small fund of $500 can prevent the need for credit when unexpected costs arise. This buffer should be separate from general savings and replenished when used. By planning for the unpredictable, families gain confidence that they can handle whatever comes their way. Avoiding these traps isn’t about perfection—it’s about creating systems that protect against emotional impulses and promote long-term stability.

Laying the Foundation for Future Financial Confidence

The financial habits formed during high school do more than manage current expenses—they shape a lifetime of money management. This period is a powerful teaching moment, offering real-world opportunities to model responsible financial behavior. When parents involve their teens in budgeting discussions, savings goals, and spending decisions, they equip them with skills that extend far beyond graduation. These experiences build confidence, discipline, and a sense of ownership over personal finances.

Teens who participate in tracking expenses, setting savings targets, or earning their own money are more likely to enter adulthood with financial awareness. They understand the cost of living, the value of planning, and the consequences of debt. These lessons reduce the likelihood of financial crises in college or early career years. More importantly, they foster independence. A young adult who has practiced budgeting is better prepared to manage student loans, rent, and credit responsibly.

For parents, the process reinforces long-term thinking. The discipline of saving for high school creates momentum for future goals like college, retirement, or home ownership. Each small victory—paying a fee without stress, avoiding credit card debt, finding a creative solution to a cost—builds confidence in financial decision-making. Over time, what once felt overwhelming becomes routine.

Ultimately, navigating high school costs is not just about money. It’s about values, priorities, and resilience. By approaching expenses with intention, seeking support when needed, and teaching the next generation through example, families do more than survive a challenging phase—they emerge stronger, wiser, and more prepared for whatever comes next. The peace of mind that comes from financial control is worth every effort invested today.